Property Risk Engineering Priorities for 2026

The Lessons of 2025, Why Preventable Losses Persist, and What We Can Do About It If building codes were the comprehensive solution to property loss, the insurance industry would be anticipating a...

The Lessons of 2025, Why Preventable Losses Persist, and What We Can Do About It

If building codes were the comprehensive solution to property loss, the insurance industry would be anticipating a quiet year. Insured loss severity is rising, and claims are growing more complex. Facilities verified as “fully code‑compliant” in 2025 still incurred seven‑ and eight‑figure losses. The problem isn’t a lack of standards; it is the assumption that compliance equates to resilience.

Property Risk Engineering Priorities for 2026 are shaped directly by lessons from 2025 and by a clear understanding of where loss-prevention efforts succeed or fail.

The Lessons of 2025

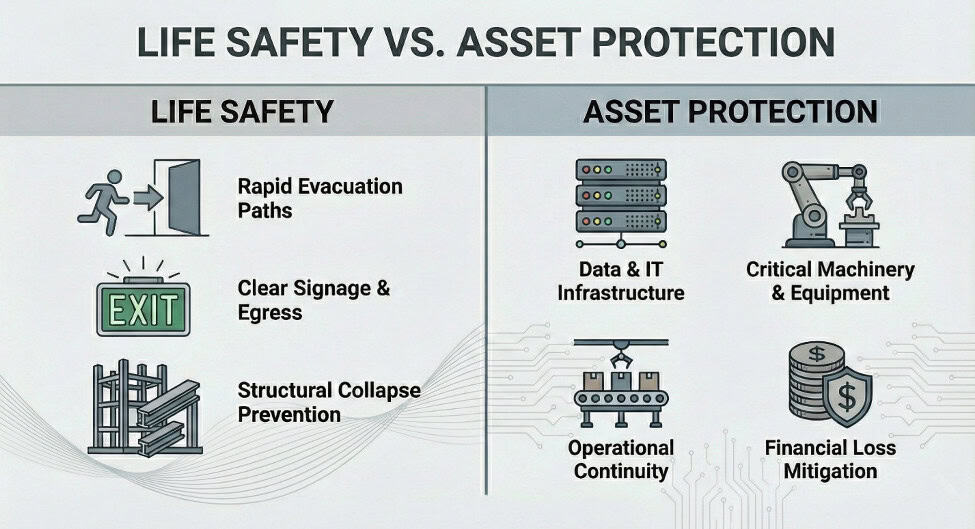

Figure 1. Modern codes prioritize life safety. Loss severity is driven by what happens after the building survives.

Life Safety vs. Asset Protection

Commercial property losses in 2025 continued to challenge the long-held assumption that modern codes equate to financial resilience. While codes prioritize life safety and prevent structural collapse, they often fail to preserve operational continuity or limit non-structural damage. As asset values rise and supply chains tighten, compliance alone is no longer a valid proxy for true risk performance.

Many properties remained structurally intact after events but suffered catastrophic non-structural damage. Envelope breaches, water intrusion, and mechanical system failures rendered facilities unusable for months. Business interruption losses escalated even where physical damage appeared limited.

The Code Gap in Secondary Perils

Figure 2. Hail damage to single-ply roof membrane.

Severe Convective Storm events emerged as a primary global loss driver, generating an estimated $69 billion in insured losses┬╣. Modern codes performed as intended for wind uplift, preventing widespread roof detachment. However, they offered limited protection against hail impact. The result was widespread destruction of code-compliant roof systems, leading to significant replacement costs and extended business interruption despite no major structural failure.

Wildfire losses followed a similar pattern. During the January 2025 Los Angeles area fires, code-driven improvements such as fire-resistant exterior cladding reduced direct flame damage. The codes did not adequately address smoke ingress, ember intrusion, or defensible space continuity. Buildings that did not burn suffered extensive contamination, loss of use, and prolonged restoration timelines.

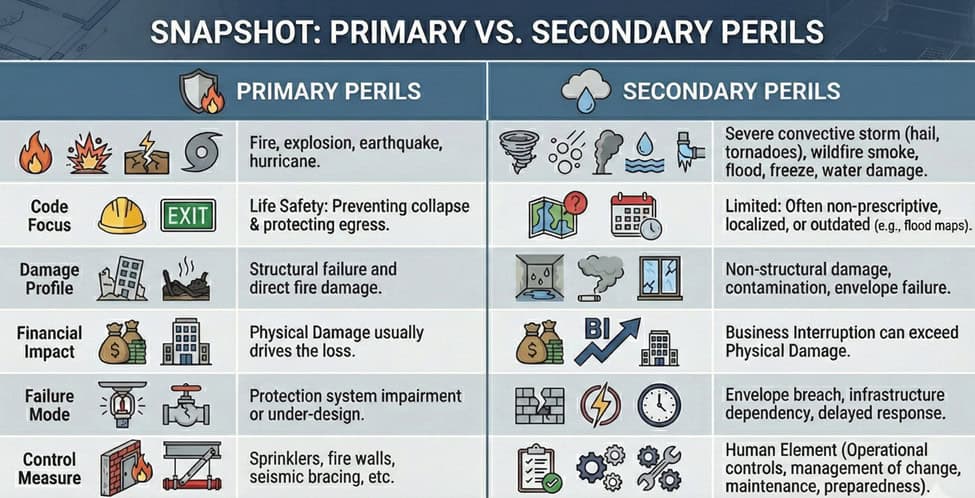

Figure 3. Table comparing primary and secondary perils

Economic Severity Multipliers

Persistently high labor and material costs amplified losses. Damage once considered minor breached retentions, affecting primary insurance layers. Inflation and higher deductibles transformed moderate events into unexpected losses.

The concentration of high-value assets increased exposure density. Data centers, automated warehouses, and specialized manufacturing facilities continued to expand into hazard-prone regions.

Market Reaction: Soft Rates, Hard Terms

Insurers responded to 2025 with a split strategy. Broadly, the market softened for well-managed risks. According to the Risk Strategies 2025 Outlook, high-quality risks saw rate reductions ranging from flat to -30% as capacity fully returned to the property sector.

Technical discipline tightened where it mattered most:

Deductibles: As highlighted in the same Risk Strategies report, insurers continued to "push for percentage deductibles for severe convective storm (SCS) perils," forcing insureds to absorb the frequency losses.

Valuation: Consistent with Alera Group’s 2025 Market Outlook, insurers maintained a strict focus on valuation adequacy, noting that "insurers remain focused on adequate insurance-to-value (ITV)" as a prerequisite for coverage.

Smoke & Physical Loss: Coverage restrictions surged around non-structural damage. This became so contentious that the California Department of Insurance issued Bulletin 2025-7 in March 2025. The Bulletin explicitly addressed the wave of denials, clarifying that "smoke damage can be covered where a policy insures against direct physical loss," thereby forcing insurers to abandon broad exclusions for contamination events.

Why Preventable Losses Persist

Despite evolving hazards and market dynamics, the underlying drivers of large property losses remain remarkably consistent.

Fire protection system performance continues to determine loss outcome. Reliability of sprinkler systems, water supplies, detection, and alarm transmission remains a decisive factor. When systems function as intended, losses are limited. When they do not, severity escalates rapidly.

Impairments in fire protection systems remain a chronic vulnerability. Planned and unplanned outages of fire protection systems continue to feature prominently in large-loss investigations. Policies exist, but enforcement and accountability commonly break down at the site level.

Water damage losses continue to dominate frequency. Aging infrastructure, freeze exposure, undetected leaks, and inadequate isolation drive losses that often exceed fire losses on an annualized basis. These failures remain a “death by a thousand cuts” for property programs.

Loss data entering 2026 does not indicate new problems. It reinforces unresolved ones.

The 2026 Playbook: Three Priorities for Resilience

If we want different results this year, we cannot rely on the same "check-the-box" compliance strategy. We need to focus on execution.

1. Prioritize Management of Change as a Survival Skill

One of the most reliable ways otherwise sound fire protection fails is through unmanaged change. Facilities evolve continuously. Fire protection systems often do not. While Management of Change is well established in process safety, it is still inconsistently applied to general property risk, leaving fixed sprinkler designs exposed to hazards that no longer resemble the original assumptions.

Losses occur when operational changes proceed without a structured hazard review, fire protection evaluation, or redesign. Increased storage heights, new packaging, automation, and layout changes quietly invalidate sprinkler design criteria. Systems that were fully acceptable at installation become under-designed over time, even though nothing appears “out of compliance.”

An effective Management of Change program establishes clear triggers for review, requires documented confirmation of protection adequacy, and grants authority to require system modification when conditions change. It also depends on coordination between engineering, operations, and maintenance, not after the fact, but before changes are implemented.

When change is intentionally managed, fire protection performance stays consistent with hazard severity. When it is not, fire losses tend to increase predictably, even in facilities that continue to meet code requirements.

2. Treat Impairment Management as a Measurable Metric

Impairment management remains one of the most effective levers for reducing fire loss severity. It is also one of the most inconsistently executed.

Programs fail not because guidance is unclear, but because accountability is unclear. Common breakdowns include delayed notifications, extended impairment duration, and inadequate temporary protection.

In many loss scenarios, protection systems were impaired for routine maintenance or construction. The impairment was documented, but the risk was not actively managed. Temporary controls were insufficient. The impairment outlasted the work.

Effective impairment management programs treat impairments as time-critical risk events. They require centralized tracking, defined authority to halt work, escalation protocols, and formal verification of reactivation.

Shortening the duration of impairment and improving the reliability of temporary protection materially reduces loss severity. This correlation is well established and repeatedly validated by loss experience.

3. Reframe Water Damage as a First-Order Property Risk

Water damage remains the most frequent and yet one of the most preventable sources of property loss. However, it often receives less attention than fire risk.

Loss drivers include aging piping, freeze exposure, mechanical failure, and undetected leaks. High-value interior finishes and equipment amplify severity.

Effective controls are readily available but underutilized. Strategies such as zoning water supplies to limit the spread of losses and installing leak detection systems for early detection can significantly reduce severity. Seasonal readiness programs address freeze exposure before losses occur.

Organizations that apply the same discipline to water risk as to fire risk consistently outperform peers in loss frequency and severity.

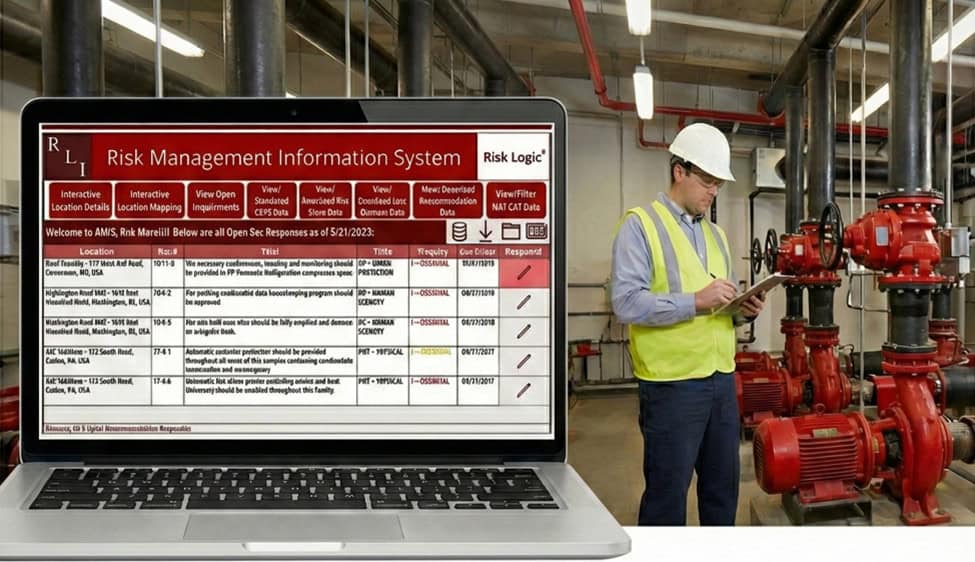

Beyond the Dashboard: Why Models Can’t Replace "Boots on the Ground"

Figure 4. Analytics inform risk decisions, but field verification confirms system capability.

In 2025, portfolio analytics and AI modeling reached new heights of sophistication. Yet these tools remain incomplete without field intelligence. While a desktop assessment can identify broad exposure patterns or a general flood zone, it cannot validate the physical condition of a fire pump, the discipline of a site’s impairment program, or the actual reliability of aging protection systems.

Effective property risk programs in 2026 integrate field-verified data with high-level analytics. They recognize that risk intelligence not grounded in physical observation creates a dangerous "transparency illusion." Engineering judgment and the ability to see how operations and protection systems interact in real time remain the only way to prioritize capital spend and avoid the assumption-based losses that defined 2025.

Conclusion: Capability Over Compliance

As 2026 begins, the lesson is not that standards have failed, but that standards alone are insufficient. Most large commercial property losses remain preventable. They occur not necessarily because the code was flawed, but because of a lack of discipline in execution, a failure to verify functionality, or a disconnect between operations and engineering.

Organizations that stop asking "Does this meet code?" and start asking "Will this survive the event?" will be the ones that weather this year with their balance sheets intact. To close the gap between assumed compliance and actual readiness, Risk Managers should evaluate their portfolios against these five criteria:

5 Questions for Every Risk Manager in 2026

Are we managing risk based on verified field conditions, or are we betting on assumed outputs?

Has our operational growth quietly outpaced our protection design? (e.g., higher storage, new automation, new packaging)

Do we treat fire protection system impairments as minor paperwork or as critical survival events?

Can our current cash flow absorb the deductible if a 'secondary' peril hits an undervalued asset?

Will our aging infrastructure perform today, or are we relying on an acceptance test from 15 years ago?

Bridging the Gap Between Compliance and Performance

As 2026 begins, the difference between a near-miss and a significant loss will not be found in a desktop model. It will be found in the operational reality of your facilities.

Risk Logic supports property owners and insurers by providing field intelligence that software cannot capture. We do not just run analytics. We put experienced engineers on site to validate protection, challenge design assumptions, and ensure your critical assets can survive the actual loss events of this year.

Stop relying on assumptions. Engage Risk Logic to ground-truth your property risk program and align your protection with performance.

References

(1) Natural Catastrophe and Climate Report, Gallagher Re - Q3 2025 - https://www.ajg.com/gallagherre/-/media/files/gallagher/gallagherre/news-and-insights/2025/october/natural-catastrophe-and-climate-report-q3-2025.pdf

Risk Strategies State of the Insurance Market: 2025 Outlook - https://www.risk-strategies.com/state-of-the-insurance-market-2025-outlook-property

Alera Group's 2025 Property and Casualty Market Outlook - https://cloud.aleragroup.com/market-outlook-25/

California Department of Insurance issued Bulletin 2025-7 - https://www.insurance.ca.gov/0250-insurers/0300-insurers/0200-bulletins/bulletin-notices-commiss-opinion/upload/Bulletin-2025-7-Insurance-Coverage-for-Smoke-Damage-and-Guidance-for-Proper-Handling-of-Smoke-Damage-Claims-for-Properties-Located-in-or-near-California-Wildfire-Areas.pdf

Read more in: